Key Info (as of April 9, 2022):

- Circulating Supply — 13,679,256.51 AAVE

- Total Supply — 16,000,000 AAVE

- Sector — Lending

- Token Type — ERC-20

- Token Usage — Governance

- Foundation date — January 5, 2017

- ATH — $666.86

- ATH Date — May 18, 2021

Overview

What is Aave?

Aave is an open-source decentralized finance (DeFi) protocol that allows users to lend and borrow cryptocurrencies with variable or stable interest rates. Lenders earn interest by depositing cryptocurrencies into liquidity pools, while borrowers can use their crypto as collateral to take out loans by using these pools. The protocol algorithmically decides the interest rates for borrowers and lenders, depending on the funds available in the pools. Aave also provides access to flash loans, which are designed to be integrated into other services.

Aave was initially running exclusively on the Ethereum blockchain, but currently the project is considered a multichain platform. In addition to Ethereum, Aave is integrated with Polygon, Avalanche, Fantom, Arbitrum, Optimism, and Harmony.

Aave has a native token called AAVE. It is an ERC-20 token that is primarily used for governance.

At the time of this writing, Aave has one the highest total value locked (TVL) among DeFi platforms. According to DeFi Pulse, the platform’s TVL currently exceeds $11 billion.

A Brief History of Aave

Aave’s origins go back to 2017 when Finnish programmer Stani Kulechov and his team developed ETHLend. The idea behind ETHLend was to enable users to lend and borrow cryptocurrencies with each other, by posting loan requests and offers on the platform. ETHLend is known as the first DeFi protocol that offered peer-to-peer lending.

In November 2017, ETHLend held an initial coin offering (ICO) for $16.2 million. The project sold 1 billion native LEND tokens during this period. But when the cryptocurrency market entered 2018 bear conditions, the project faced a lack of liquidity, and difficulty matching loan requests and offers. In September 2018, ETHLend was rebranded to Aave, which means “ghost” in Finnish.

On January 8, 2020, the Aave V1 mainnet was launched on the Ethereum blockchain. It introduced the main Ethereum market with traditional ERC-20 tokens, and the Uniswap market, where users were able to use Uniswap V1 liquidity pool tokens as collateral. In October 2020, migration from the LEND token to the AAVE token took place at a ratio of 100:1.

In December 2020, the Aave V2 mainnet went live. The updated version added risk management tools and optimized transaction fees. In addition, Aave started supporting the Polygon market on the Polygon sidechain.

In January 2022, Aave launched permissioned lending and a liquidity service called Aave Arc for institutional investors. In March 2022, Aave deployed Aave V3 protocol.

How Does Aave Work?

Lending/Borrowing Mechanism

There are two types of market participants on the Aave platform, lenders and borrowers.

Lenders are users who deposit assets into Aave and receive “aToken” with a ratio of 1:1 to the asset they deposited. aToken is an interest-bearing token that is pegged to the value of the underlying asset, so lenders can redeem the aToken 1:1 for the original asset they deposited. The lender’s aTokens balance grows, reflecting the interest paid by borrowers of the asset. Lenders also receive fees from flash loans.

Borrowers deposit assets into Aave to be used as collateral, but they can only borrow a smaller value than deposited collateral. That is because of the “overcollateral” concept, which allows Aave to remain solvent. The borrowing power of the collateral is determined by the Loan-To-Value (LTV) ratio. This depends on the volatility as well as the other risk parameters of the collateral asset.

For example, if the LTV for borrowing LINK is 80%, for each 1 LINK in collateral, the maximum a user can borrow is an amount equivalent to 0.8 LINK. The loan/value of the collateral ratio is calculated individually for each collateral type, and is expressed as a percentage.

Borrowers who want to close the debt must return the borrowed assets plus interest. As long as there is debt, the collateral value is locked in the protocol.

Source: Coin98 Insights

One of the unique features of Aave is that it allows borrowers to switch between fixed and floating interest rates. In most cases, interest rates in DeFi are volatile, making it difficult to estimate the long-term cost of borrowing. But with Aave, users can switch the rate, in an attempt to decrease borrowing costs. Usually, when borrowers anticipate interest rates to rise, they switch from a floating rate to fixed rate, and vice versa. However, if the lender’s earning rate for the asset increases above the fixed borrow rate, the fixed rate can be rebalanced to the “new fixed rate.”

At the moment, Aave supports:

- 22 assets on Aave V1

- 34 assets on the Ethereum V2 market

- 7 assets on the Ethereum V2 AMM market

- 13 assets on the Polygon V2 market

- 16 assets on the Polygon V3 market

- 7 assets on the Avalanche V2 market

- 8 assets on the Avalanche V3 market

- 8 assets on the Optimism V3 market

- 8 assets on the Harmony V3 market

- 8 assets on the Arbitrum V3 market

- 10 assets on the Fantom V3 market

Liquidation and Risk Mitigation

The liquidation mechanism relies on a so-called health factor (HF). It expresses the safety of the user’s assets related to the borrowed asset, and its underlying value. The higher the health factor, the safer the asset. If the health factor increases, then the risk of liquidation is lower. In case of a sharp drop of the indicator, the user can fully or partially repay the loan or deposit additional collateral. When HF drops below a certain level, it means liquidation of the loan.

It is possible to liquidate no more than 50% of the user’s assets. The main plus of such an approach is that users can maintain part of the loan and wait for the price of collateral to rise. But if the value of collateral continues decreasing, then the risk of losing the remaining 50% increases. Price data for Aave loans comes from Chainlink oracles.

Source: Aave documentation

If the liquidation process is not completed, loans can become undercollateralized, forming problematic debts. For such situations, Aave protocol may use a risk mitigation mechanism called Safety Module. It contains an insurance fund for shortfall events.

In case of a shortfall event, the funds required to refinance the deficit can be auctioned to the Backstop Module. Users can deposit stablecoins or ETH to the Backstop Module before selling in open markets. In extreme situations, users may vote for a Recovery Issuance of AAVE tokens to be auctioned to the Backstop Module first, then open markets.

Flash Loans

Flash loans are uncollateralized loans where repayment is carried out within the same block. In most cases, they are used for arbitrage, collateral swap, refinancing collateral, and rebalancing the portfolio. The Flash loan has a 0.09% fee from the borrowed value. The fees go to lenders.

Aave V2 Features

The market size of Aave V1 is currently around $100 million, while the single Ethereum V2 market has a $15 billion market size, according to the Aave website. The main reason for this difference is that the V2 protocol has a more efficient use of gas. In some cases, users can save up to 50% on commissions.

In addition, Aave supports in V2 protocol:

- Collateral swap — users can move their collateral from one token to another. It may help prevent liquidation on specific markets.

- Debt tokenization — borrowers receive tokens that represent their debt. It allows borrowers to delegate native credit.

- Batch flash loans — users can borrow several assets at the same time using flash loans.

Aave V3 Features

Aave V3 was deployed in March 2022, meaning users have just begun to discover the possibilities of the new version. Currently, Aave V3 markets have an over $50 million combined market size. This performance doesn’t include the Ethereum market which should be deployed when the community determines the maturity of the V3 markets.

In addition to risk management improvements and gas optimization by 20-25%, Aave V3 also introduced:

- Portal — allows the flow of liquidity between V3 markets across different networks

- Isolated mode — assets can be listed as isolated in Aave V3. Borrowers who supply an isolated asset as collateral cannot supply other assets as collateral

- Efficiency mode — allows borrowers to improve borrowing power when supplied and borrowed assets are correlated in price

- Multiple rewards — allows listed assets to enable additional incentives

Aave Native Token

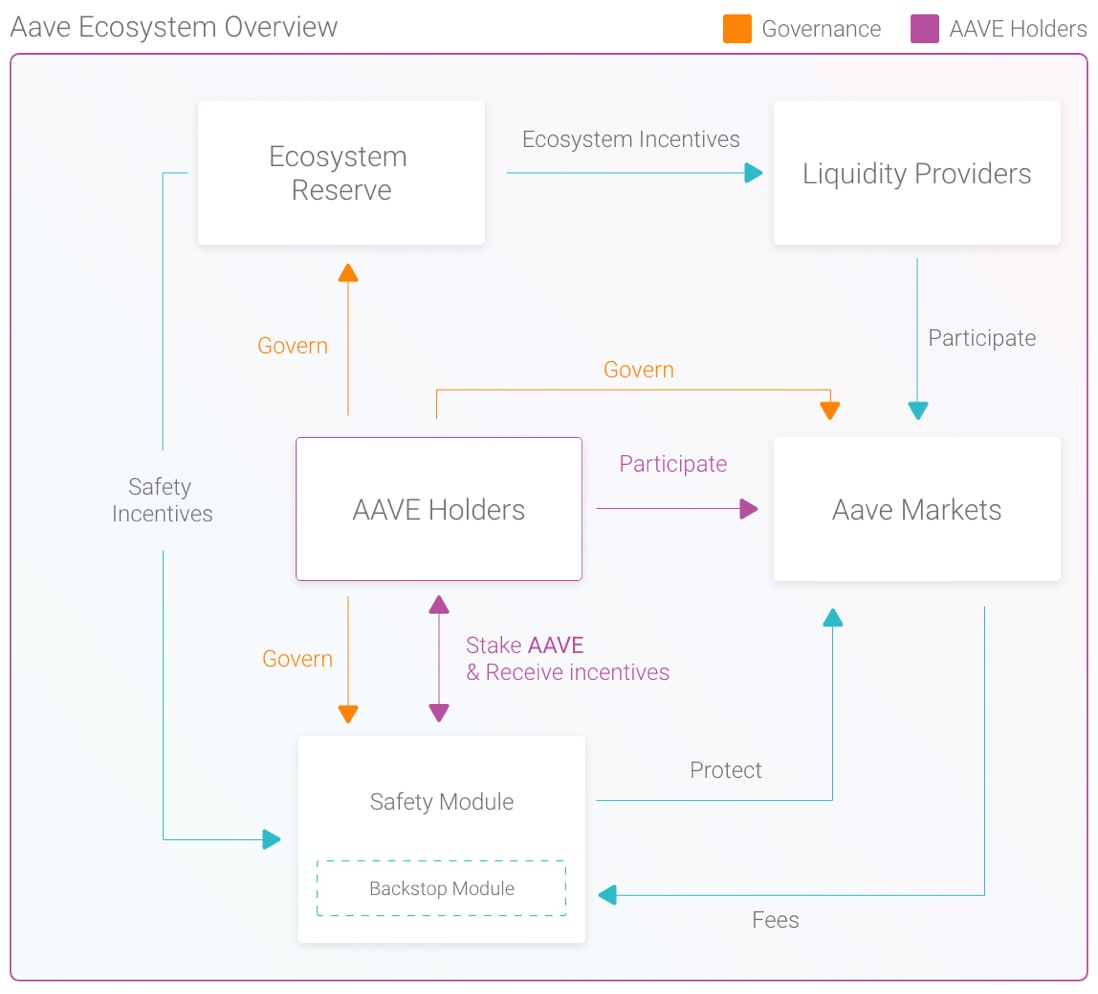

AAVE is an ERC-20 token and native to the Aave platform. After the migration from LEND to AAVE at a 100:1 ratio, 13 million AAVE tokens have been redeemed by LEND holders. The remaining three million out of the total 16 million AAVE supply are distributed to the Aave Ecosystem Reserve. It means that all AAVE tokens have already been released with an 81% to 19% token allocation ratio.

AAVE is the core of the Aave ecosystem which is called Aavenomics. Currently, AAVE can be used for:

- Staking in Safety Module

Users stake AAVE tokens in the Safety Module and receive Stake AAVE (StkAAVE) tokens in return. When users withdraw tokens from the stake, Aave is returned to them and the platform burns StkAAVE. Up to 30% of StkAAVE can be used to cover shortfalls. Every day, 550 StkAAVE are distributed as a reward to all users who stake AAVE in the Safety Module.

- Ecosystem and Safety Incentives

Safety Incentives ensure the safety of the protocol by incentivizing AAVE holders to participate in the Safety Module. Ecosystem incentives are provided to liquidity providers and liquidators to maintain sustainability in liquidity pools. AAVE holders determine how the Ecosystem Reserve should be allocated between safety and ecosystem incentives.

- Governance

AAVE tokens are used to ratify Aave Improvement Proposals (AIPs). To submit governance proposals, users first create a request for comment (ARC) and share it with the community. Such an approach is used to ensure extensive discussion before AIPs are pushed for on-chain voting. If ARC receives support from the community, it turns into AIP. So far, at least 36 ARCs have become AIPs.

Source: Github

Find out more about Aave

Aave has rapidly become one of the top DeFi projects in terms of total value locked in the protocol. The launch of Aave V2 along with Aavenomics was an enormous catalyst behind its success. But the project is still under active development, and the recent deployment of the Aave V3 protocol shows that developers continue adding new features to strengthen Aave’s position in the DeFi lending field.

With CEX.IO, you can buy AAVE instantly to open the gate to the Aave ecosystem, or trade AAVE in pairs with the U.S. Dollars and USDT.

Disclaimer: Information provided by CEX.IO is not intended to be, nor should it be construed as financial, tax, or legal advice. The risk of loss in trading or holding digital assets can be substantial. You should carefully consider whether interacting with, holding, or trading digital assets is suitable for you in light of the risk involved and your financial condition. You should take into consideration your level of experience and seek independent advice if necessary regarding your specific circumstances. CEX.IO is not engaged in the offer, sale, or trading of securities. Please refer to the Terms of Use for more details.