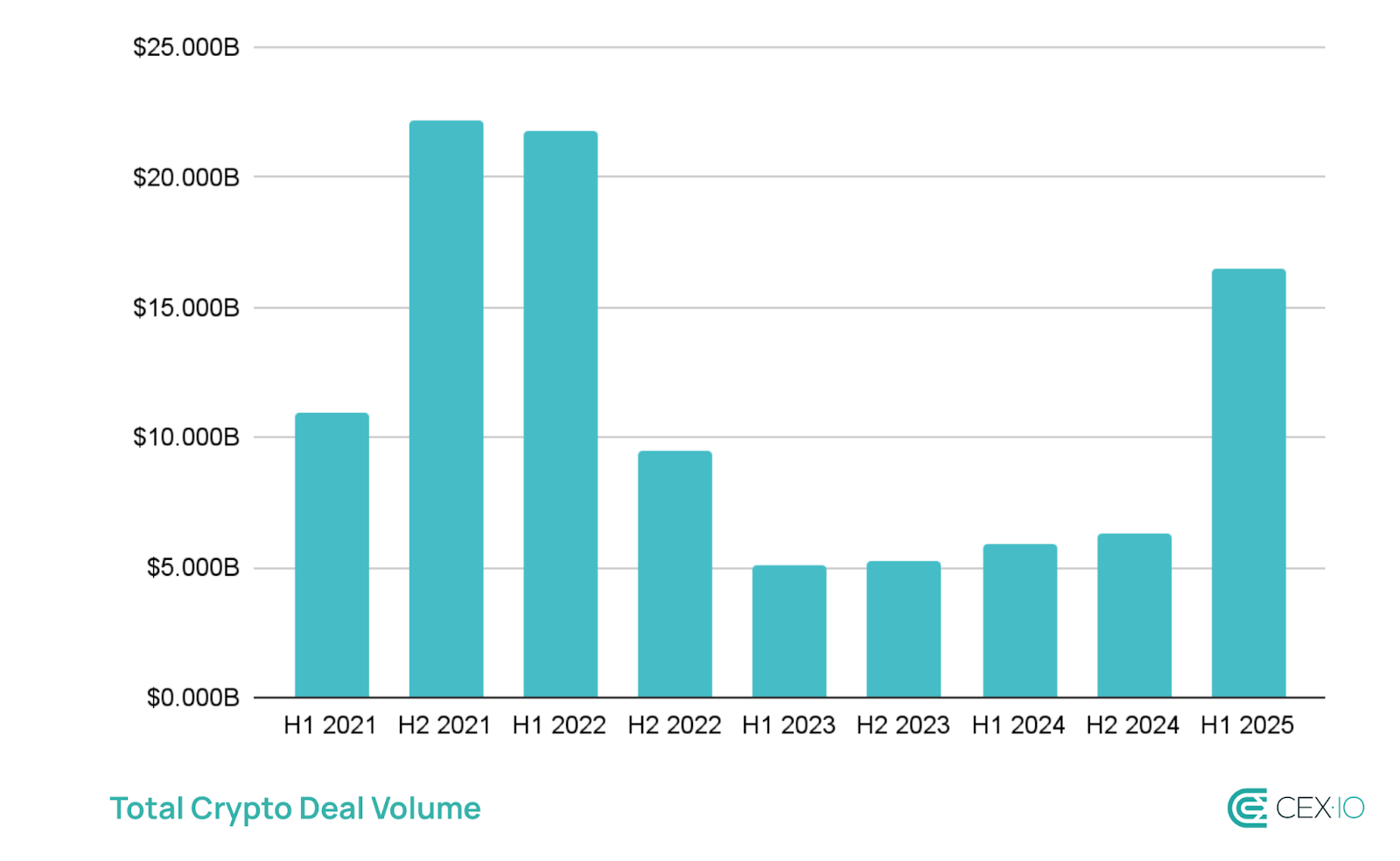

- Crypto deal volume in H1 2025 already exceeds H1 2021, the industry’s most active year to date, putting 2025 on track to be the biggest year.

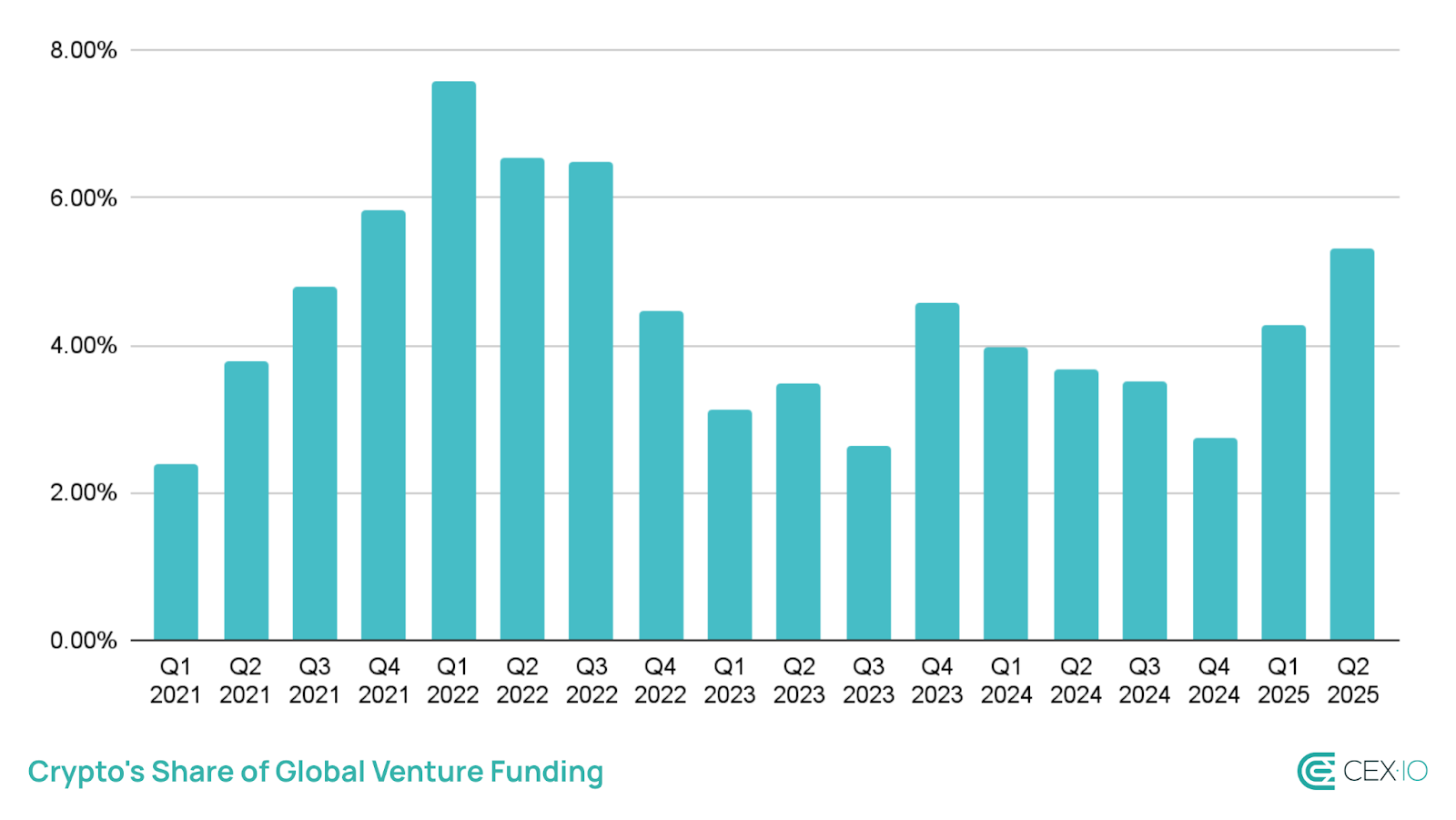

- In Q2 2025, crypto fundraising made up 5.3% of global venture funding, the highest share in three years.

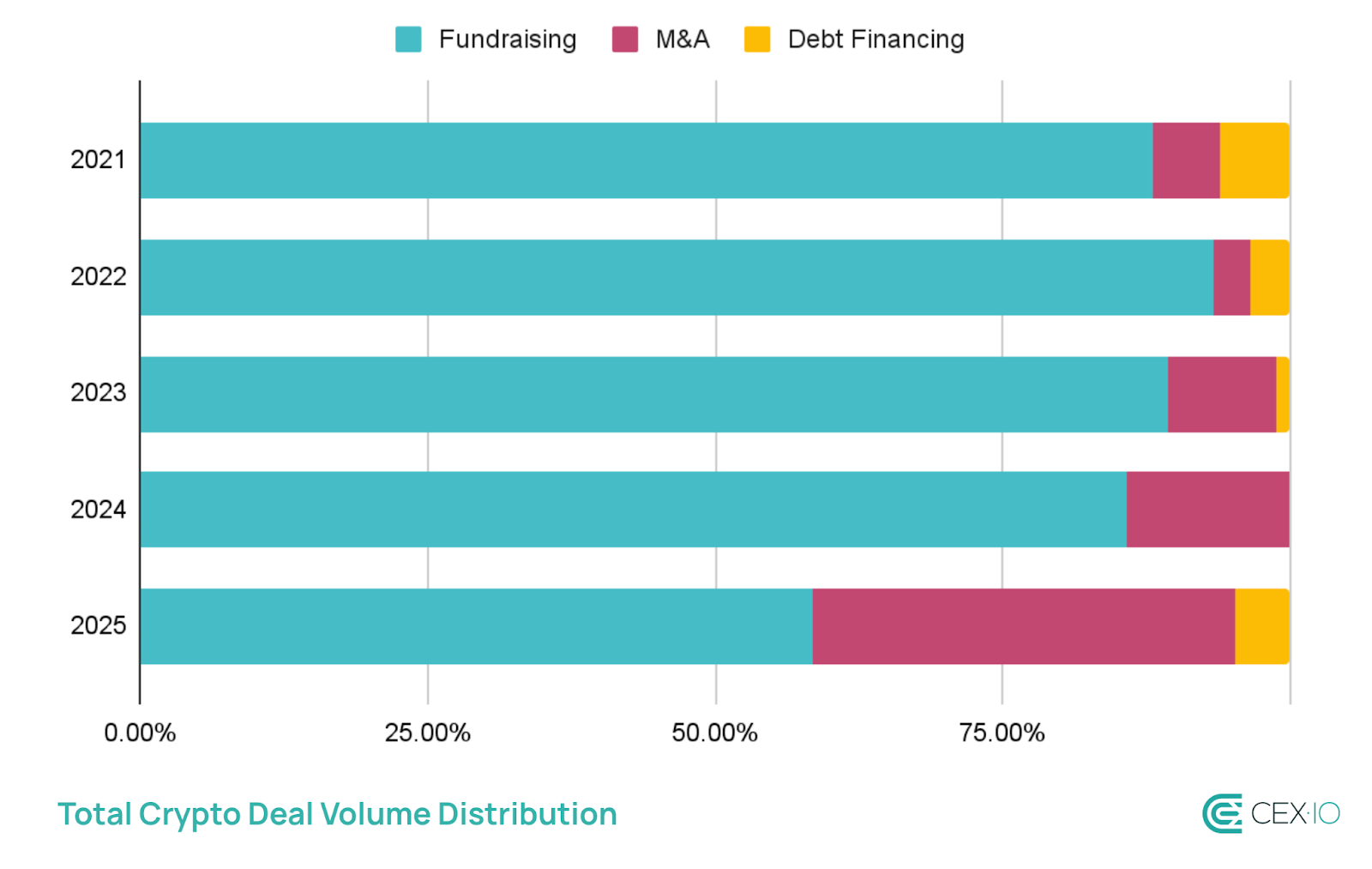

- M&A activity now makes up over one-third of all crypto deal volume, signaling a transition toward industry consolidation over early-stage funding.

- 82% of funded projects in 2025 are tokenless, reflecting a growing focus on sustainable business models over speculative token launches. In turn, 85% of token-funded projects in 2025 are currently underwater.

- AI, CeFi, and DeFi dominate fundraising volume, while interest in launching new L1/L2 networks has dropped to multi-year lows.

The crypto industry is regaining its deal-making momentum, with total deal volume reaching $16.5 billion in the first half of 2025. That’s already more than the $12.2 billion recorded during all of 2024, and ahead of the $10.9 billion seen in H1 2021, the industry’s most active year to date. If this pace continues, 2025 is on course to become the biggest year ever for crypto fundraising and M&A activity.

Below, we explore the main drivers behind this surge and which sectors are attracting the most investor interest.

General Overview

Crypto Fundraising Increased in Scale

In Q2 2025, crypto fundraising made up 5.3% of global venture funding, the highest share in three years. While total global fundraising remains below 2021’s peak, crypto’s slice of the pie has been growing steadily since U.S. elections, showing renewed investor interest in the space.

What makes this cycle especially notable is the pace of recovery. Crypto industry’s funding rebound in 2025 is outpacing its rise during the 2021 bull market, even though broader venture capital markets are showing signs of caution, and remain hyperfocused on AI. This suggests that crypto is becoming a more resilient and strategically important sector within the global startup ecosystem, not just the one that rises along with the wider IT sector.

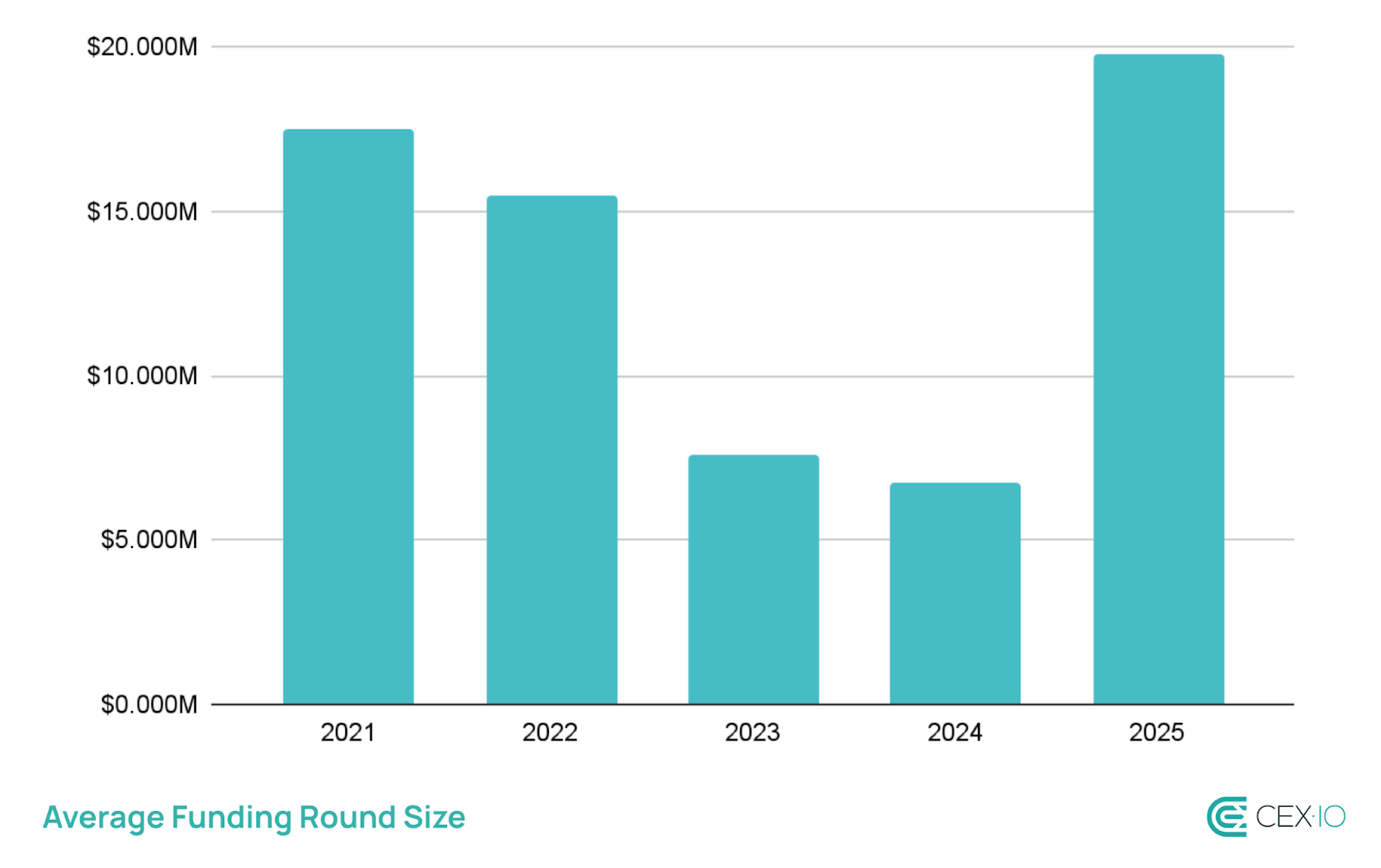

As such, venture capital remains the biggest part of crypto deal-making in 2025. But this year brought a key change: instead of many small funding rounds, fewer projects are raising larger sums. While the number of deals is down compared to previous years, the average round has grown to nearly $20 million, which is a sharp rebound from the post-2022 dip.

This shows that investors are being more selective, choosing to back teams with stronger fundamentals or clear growth potential, rather than spreading capital thinly across many early-stage ideas.

M&A Activity Becomes a Driving Force

One of the biggest shifts in 2025 has been the rapid rise in M&A volume. Mergers and acquisitions have already surpassed $6 billion, more than triple last year’s total. M&A now accounts for 36.7% of total crypto deal volume, the highest share ever.

This rising share suggests a maturing market. Instead of just funding new projects, companies are now buying existing ones to gain technology, teams, or user bases. It’s a sign that growth in crypto is increasingly being driven by consolidation and strategic expansion, not just by innovation from scratch.

A Tokenless Trend Gains Ground

Another major trend in 2025 is the move away from token-based fundraising. So far this year, 82% of projects that raised money did so without launching or using a native token, which is a big change from previous cycles when tokens were central to most funding strategies, especially during the ICO boom.

This shows that both investors and founders are now more focused on building real products and generating revenue, rather than relying on tokens to drive hype. And that caution seems justified: 85% of token-funded projects in 2025 are currently showing negative performance, either year-to-date or since launch.

The move toward tokenless fundraising could also be viewed as an additional sign of market maturing, with investors putting money into teams that prioritize strong business foundations before potentially launching a token.

What Crypto Sectors Show the Highest Investor Interest

As crypto deal activity picks up, the distribution of capital across sectors shows both familiar leaders and new areas of growth.

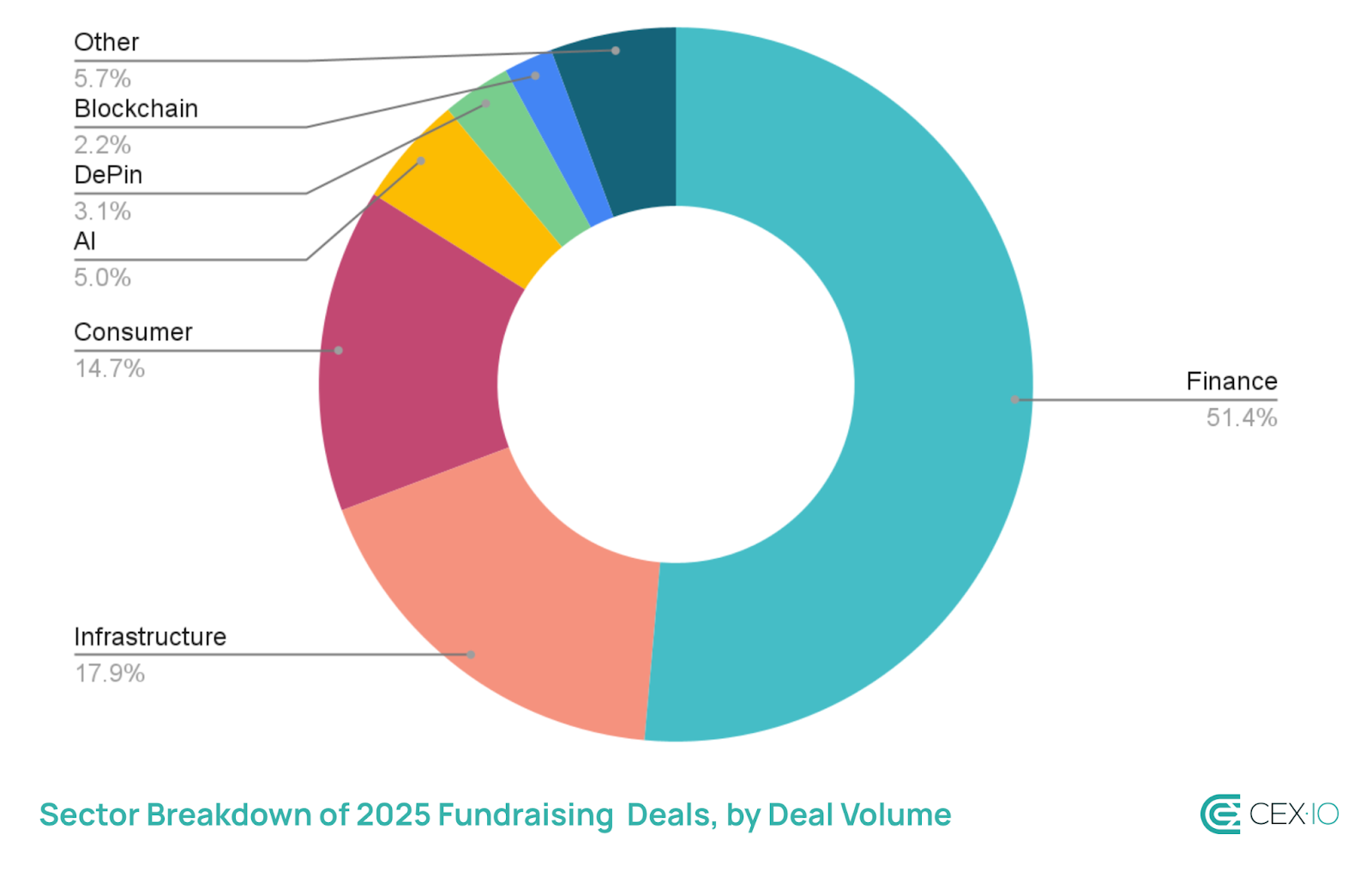

Fundraising

Finance remains the top category in fundraising, attracting nearly $4.9 billion across 171 deals. This broad category includes investments in both CeFi and DeFi projects, and their dominance in fundraising is in line with past cycles.

As for other categories, here are key highlights:

- Infrastructure fundraising, which includes hardware, security, bridges, and oracles, was boosted by big deals in the mining sector. Companies like Bitmain and TWL Miner raised major rounds in Q2.

- The Blockchain sector, covering new L1 and L2 networks, saw a dramatic contraction. Once accounting for 10-20% of fundraising, it now makes up just 2% of deal volume. This suggests that investor appetite for launching new networks is at a multi-year low.

- AI-focused crypto projects have been steadily increasing their share of fundraising every year since 2021. This rapid expansion suggests that AI might be playing a bigger role in the crypto landscape in future cycles.

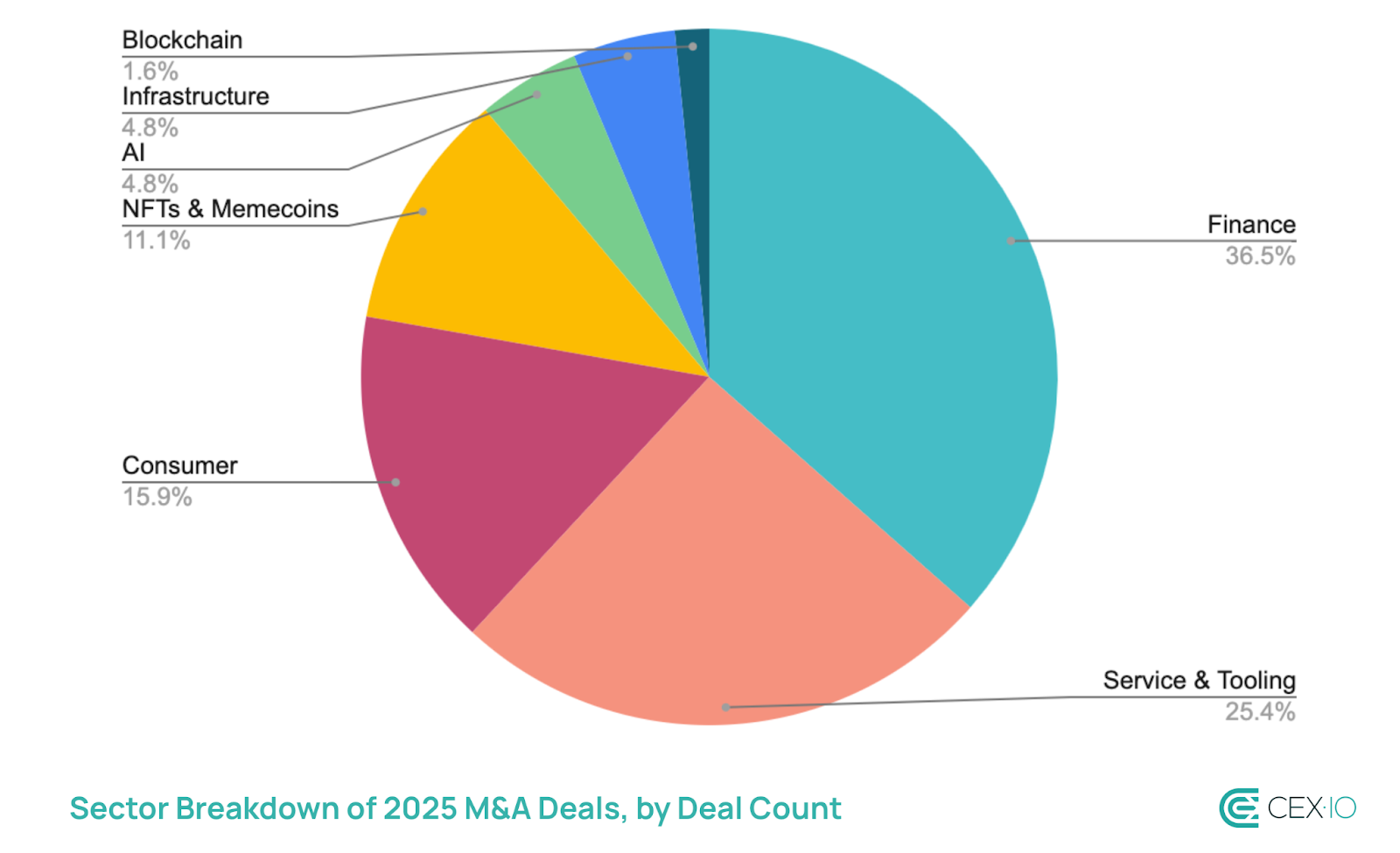

M&A

M&A data is less transparent than fundraising. While there have been 63 M&A deals so far in 2025, about 86% of them did not disclose the transaction amount, making it difficult to estimate the true value of the sector’s activity. However, most of the known deals are in the Finance sector. Notable examples include Coinbase purchasing Deribit, Kraken acquiring NinjaTrader, and Ripple buying Hidden Road.

In terms of deal count, Finance leads with 23 acquisitions, followed by the Service & Tooling category, which includes developer platforms, compliance tools, and analytics providers. Consumer apps such as gaming, wallets, and social platforms rank third in M&A activity.

Final Thoughts

The boom in crypto fundraising and M&A in 2025 is more than a sign of recovery, it highlights the direction the industry plans to move forward. Capital is flowing to fewer but stronger players, M&A is becoming a core strategy, and tokens are no longer a default requirement for early-stage success. The next wave of crypto may be less about explosive innovation and more about refining, scaling, and integrating what’s already been built. This quieter, more strategic cycle could lay the foundation for deeper, more sustainable growth — one that looks less like a hype-driven sprint and more like a long-term build-out of global infrastructure.

Sources

The data used for this research consists of publicly available information from RootData, Blockworks Research, Crunchbase, Coingecko, and Coinmarketcap. The observation period for this study was focused on 2021-2025 for general overview, and 2025 for sector and token overview, with data points ending July 8, 2025.

The web content provided by CEX.IO is for educational purposes only. The information and tools provided neither are, nor should be construed as, an offer, or a solicitation of an offer, or a recommendation, to buy, sell or hold any digital asset or to open a particular account or engage in any specific investment strategy. Digital asset markets are highly volatile and can lead to loss of funds.

The availability of the products, features, and