Bitcoin momentarily lost its 2021 bull market support by dropping to $26,000 on May 12. Since then, it has climbed back to $30,000 and has been consolidating around that price level.

However, Bitcoin is far from being out of the woods since there is no substantial support until the previous all-time high price at $20,000 if the current $28,000-$30,000 range is lost. A major point of concern is that although the US dollar index is undergoing a correction right now, there has almost been no reaction in the price of Bitcoin, which hints at the weakness in Bitcoin’s trend.

Outflows from altcoins are also continuing following the UST/Terra debacle. Ethereum started to underperform Bitcoin for the first time since the 2018/19 bear market hinting at a new uptrend in the dominance of Bitcoin. Despite Tether’s recently published audit report which confirms its claimed $82 billion reserves, confidence in altcoin and stablecoin markets remains low.

In this issue of the crypto ecosystem update, we will discuss the exchange inflows of Bitcoin, as well as the Bitcoin fear & greed index and a brief technical analysis. We will also provide an update on Ethereum and the UST/Terra ecosystem, along with Tether’s recent audit.

Bitcoin deposits to exchanges

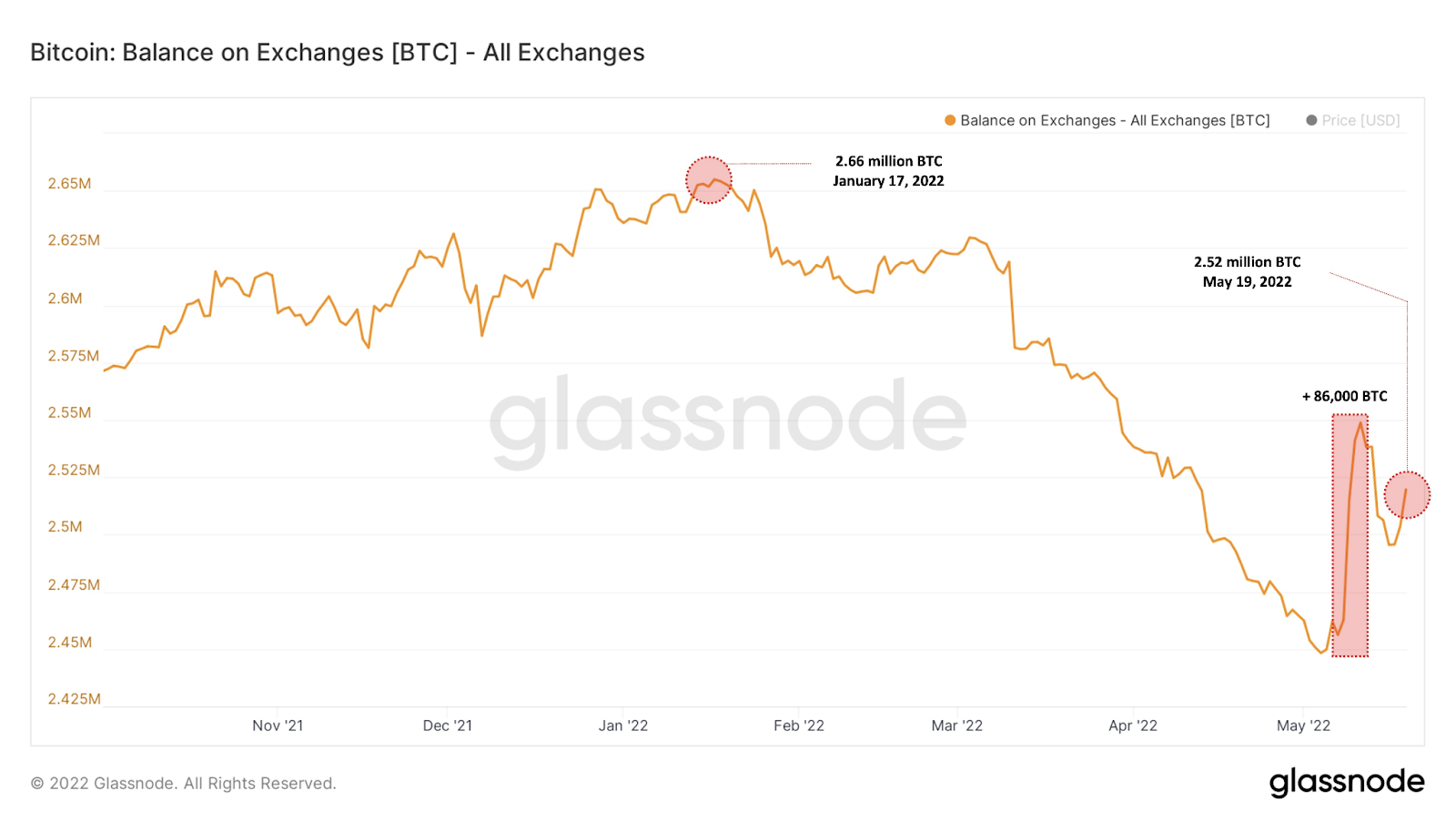

Following the UST stablecoin’s de-pegging on May 8, the Luna Foundation Guard (LFG), a non-profit organization that backs the Terra blockchain ecosystem, sold all of its Bitcoin reserves (80,394 BTC) to defend UST’s peg. This meant depositing bitcoins to cryptocurrency exchanges. As you can observe in the chart below, exchange balances surged by as much as 86,000 bitcoins from their early May bottom levels.

Source: Glassnode

Increases in exchange inflows can suggest that investors are interested in selling their Bitcoin holdings by depositing them to exchanges. This generally happens shortly before and after cycle tops, as well as before capitulation events.

Although the Bitcoin balance on crypto exchanges has been declining since January 2022, the sudden turnaround in May triggered by the LFG sell-off may catalyze a new uptrend unless market sentiment turns positive soon. Since May 2022 does not correspond to a Bitcoin cycle top, this potential new uptrend in the BTC exchange balance may open the gates for a new Bitcoin downtrend.

Bitcoin Fear and Greed Index

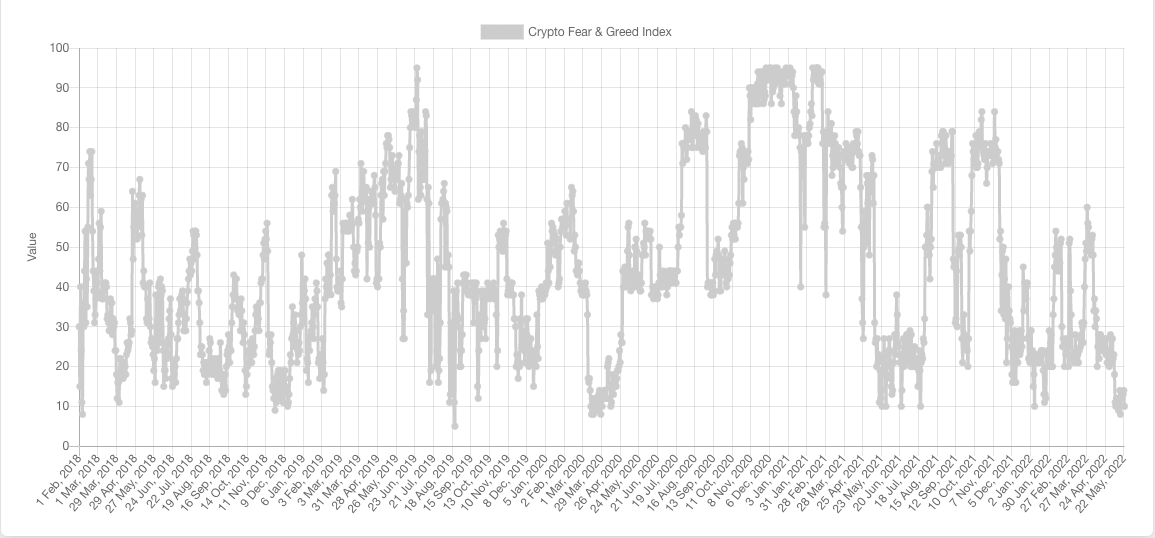

Bitcoin’s fear and greed index measures market sentiment. Extreme greed usually precedes cycle tops while extreme fear precedes market bottoms.

Source: Alternative.me

The Fear and Greed Index is currently at ten which corresponds to a historically low level and means extreme fear. As you can see in the chart below, this index almost always bottomed out at ten during the last four years. This suggests that there is a market structure at this level and that the Bitcoin bottom or capitulation could be very near if it has not bottomed out already.

Source: Alternative.me

Bitcoin price analysis

During the peak of the UST/Luna crisis, Bitcoin fell to as low as $26,000. Whether Bitcoin has another leg down largely depends on the already deteriorated market sentiment, as well as the next movement of the S&P 500 stock index.

- S&P 500 stock index

If the S&P 500 stock index in the U.S. closes a trading day below the critical 3,850 support, it could trigger a sell-off to the next major support at 3,230 as you can observe in the charts below.

This would mean a further 17% drop from the current price, which could, historically speaking, create as large as an approximately 30% drop in Bitcoin’s price.

S&P 500 daily price chart. Source: Tradingview

The index fell to as low as 3,810 on Friday, May 20 but managed to close the day above 3,900. The S&P’s moves will be very critical this week which could also impact the cryptocurrency market.

- Bitcoin’s short-term structure

In the meantime, Bitcoin needs to protect its short-term market structure at $28,700.

A four-hour closing below this level, if accompanied by new negative developments among cryptocurrencies and sell-offs in the S&P, could trigger panic in the market and cause capitulation for Bitcoin.

Bitcoin/U.S. Dollar price chart on a 4-hour time frame

- Overbought daily stochastic RSI

During bear markets, momentum indicators can get quickly overbought on higher time frames, like the daily time frame. Despite falling from $42,000 on April 21 to $26,000 by May 12, Bitcoin’s stochastic RSI has already become overbought on the daily chart with a mere 15% bounce from the $26,000 bottom (see the chart below).

This is typical bear market behavior in cryptocurrencies which could suggest that Bitcoin’s recent bounce may be nearing a top soon and that the price may not be able to break above its current horizontal range (the $32,000 resistance) as it runs out of further momentum.

Bitcoin/U.S. Dollar daily price chart with the stochastic RSI indicator

- The US Dollar index

The US Dollar index, DXY, was rejected at the 105 resistance level on May 13 and the price has been dropping since then. Although the index fell to 102 very rapidly on the week of May 16, Bitcoin showed almost no reaction in the meantime. Normally, such a steep drop in the DXY would trigger a 20-25% rally in the Bitcoin price. Instead, Bitcoin could only range horizontally between $29,000 and $31,000 with its daily stochastic RSI already becoming overbought.

This suggests that the Bitcoin trend is weak and that it may have difficulty breaking out of its current horizontal range to the upside.

Ethereum price analysis

Ethereum performed much better than Bitcoin during 2021, generating as much as four times more returns as of December 2021.

So far in 2022, Ethereum has failed to reach the 0.1 historical resistance in terms of the Ethereum/Bitcoin price parity. It also could not break out of the rising channel that it has been following for over a year (see the chart below).

Rising channels are often confused with bull flags because they also have a pole. However, in bull flags, the flag is tilted downwards while rising channels face upwards, which are more likely to break downwards during a macro downtrend.

During Bitcoin’s March 2022 rally, Ethereum failed to increase more than Bitcoin and made a lower high price on the Ethereum/Bitcoin chart (circled in orange in the chart below).

Ethereum/Bitcoin parity chart on a weekly timeframe

The Ethereum/Bitcoin parity is at the very bottom of the channel support now. Losing the channel support due to a Bitcoin crash or another black swan event could cause the parity to start a new, stronger downtrend that could go as low as the next major support at 0.04.

Ethereum/Bitcoin parity chart on a daily timeframe

Ethereum recorded a highly bearish rejection candle on May 11 just when it was attempting a breakout to the upside (see the chart above). The UST/Luna debacle brought a sudden and strong sell-off on the Ethereum/Bitcoin parity. Such strong rejections during the same trading day often initiate a new, stronger trend to the downside.

Given the current outlook of the altcoin market as a consequence of the UST/Terra turmoil, tides may be turning for Ethereum unless the ongoing merge of the Ethereum blockchain creates a positive catalyst and new excitement in the market.

The proposed Terra fork

Luna printing stopped on Friday, May 13 after 6.5 trillion tokens were put into circulation and the token price bottomed out at around $0.00001. Since then, debates to save the Terra ecosystem have been flooding the crypto space.

Voluntary coin burns by individual investors, compensating small investors from the Luna Foundation Guard, and issuing a new stablecoin backed with real assets are some of the suggestions that have been made.

The most recent discussion to revive the project is to create a fork of the Terra blockchain.

Terra’s CEO and co-founder Do Kwon has recently proposed forking the Terra network into a new chain.

According to the proposal, the fork would create one billion new tokens to distribute among investors to incentivize them to stay in the Terra ecosystem whereas the old chain would become known as “Terra Classic” and the original Luna tokens would become “Luna Classic”.

Terraform Labs is currently having a poll to measure the investor sentiment towards a fork of the existing blockchain. According to the poll’s results thus far, 65% of the voters voted in favor of the fork.

On the other hand, a recent vote on Twitter shows a contradictory outcome to the Terra forum poll. The vote asks the Luna community whether they want to fork Terra or burn Luna tokens and 93% of the respondents so far have voted in favor of a Luna token burn.

Whether the Terra management will heed the Terra community or the Twitter community, or come up with another solution remains to be seen in the coming days.

Tether’s recent audit report

During the chaos of the UST’s de-pegging news, the market also became fearful of Tether’s peg which caused the largest stablecoin to temporarily lose its peg. The size of the Tether (USDT) market cap was four times larger than that of UST, so a meltdown in the value of USDT poses a much more serious risk to the cryptocurrency market’s existence.

Unlike UST though, the de-pegging of Tether was a short-lived one. Although the value of USDT briefly dropped to a low of $0.96, it recovered within 36 hours.

To protect the $1 peg, the Tether team announced on May 12 that verified customers can redeem their US Dollar deposits from the Tether treasury in return for USDT tokens they hold. So far, $8 billion worth of USDT has been redeemed and removed from circulation which dropped the total USDT supply from $82 billion to $74 billion.

With the cooling down of the UST crisis, USDT redemptions also came to a halt securing the Tether ecosystem for now. To regain the confidence of its investors and the overall cryptocurrency market, the Tether management also released an audit report that verifies its consolidated reserves.

The audit report may come as a relief to USDT holders as there has been a lot of uncertainty about how Tether backs itself. This was exacerbated by the SEC’s subpoenas in the past and the high ratio of less liquid commercial papers in Tether’s reserves as of the end of 2021.

According to the audit conducted by the independent accounting firm, MHA Cayman, the total assets of Tether Holdings are at least $82,424,821,101, which is significantly higher than the value of issued USDT digital tokens in circulation ($74 billion). This means Tether’s reserves against issued digital tokens exceed the amount required to redeem them.