Reductions in interest rates during the climax of the COVID-19 crisis in 2020 dropped the cost of leveraging to historic lows. This incentivized people to take loans and leverage their investments so that they could maximize profits without having to liquidate their assets.

Cryptocurrencies benefited greatly from this abundant liquidity in the financial markets. The introduction of debt markets in cryptocurrencies paved the way for the decentralized finance (DeFi) industry to seize a greater share of the investment landscape. The value of funds locked in different DeFi applications and protocols exploded from a mere $600 million in January 2020 to as high as $180 billion in December 2021.

Since the Federal Reserve started raising fund rates in March 2022 due to surging U.S. inflation, an enormous deleveraging took place in the crypto DeFi industry. As the cost of leveraging has become more expensive, the demand in the crypto market has shifted towards relatively risk-off assets that are not part of the DeFi space.

As a consequence, the total value locked (TVL) in DeFi products dropped to a low of $52 billion on June 19, shedding 71% from the value highs reported in December 2021. The TVL decline is a function of both falling token valuations, as well as the reduction in aggregate leverage.

Below are the TVL drops in percentages for different DeFi products during the second quarter of 2022:

- Decentralized exchanges (DEX): -63%

- Lending & borrowing platforms: -71%

- Yield farms: -68%

- Liquid staking: -76%

DEXs constitute the largest category in the DeFi space at $23 billion TVL as of June 30, while lending & borrowing platforms had $15 billion TVL on the same date. Yield farms and liquid staking are two of the smaller categories in DeFi, with $6.5 billion and $5.5 billion TVL respectively as of June 30.

In this article, we will review the notable crypto ecosystem events in the first half of 2022 that continue to shape DeFi space.

The collapse of UST and Terra

The collapse of the Terra protocol and its native algorithmic stablecoin, UST, was the most impactful event in the DeFi industry during the second quarter of 2022.

A total of $30 billion value just evaporated within a few days in May 2022, which then created a domino effect across the whole ecosystem. Forced liquidations and bankruptcies snowballed until they reached a $52 billion TVL dip on June 19.

UST’s de-peg

Following the Fed’s rate hike announcement on May 4, the price of Bitcoin started to drop rapidly. UST was backed with Bitcoin reserves worth $1.6 billion, so a meltdown in reserves caused panic among UST holders who rushed to sell their tokens to other stablecoin products.

An unknown user on Binance sold $84 million of UST to other stablecoins while the same wallet reportedly swapped a total of 285 million UST on decentralized platforms like Curve and Anchor.

Such large sell-offs eventually broke UST’s peg against the US Dollar on May 8 and there was not much interest left among arbitrageurs to preserve the value of UST.

Hyperinflating the LUNA supply

To counter the massively rising UST supply in circulation, the Luna Foundation Guard (LFG), a non-profit organization that backs the ecosystem, started to buy UST by depleting the BTC reserves. A wallet address publicly associated with Terra shows that the roughly 71,000 BTC in the reserves was exhausted trying to save UST (only 313 BTC are present in the wallet today).

However, the market was already swamped with so many UST tokens that neither the depletion of reserves nor the arbitrage efforts of traders were enough to restore the peg. As a final measure to save UST, the Luna Foundation Guard chose the path of hyperinflating the LUNA token supply.

By the nature of the protocol’s design, the price of UST is algorithmically backed by LUNA tokens. LUNA holders have the right to mint 1 UST for every $1 worth of LUNA they hold. When UST is minted, an equivalent amount of LUNA tokens is burnt and taken out of circulation.

Similarly, UST holders have the right to mint a corresponding amount of LUNA tokens for every UST they hold, which would in return remove the UST out of circulation.

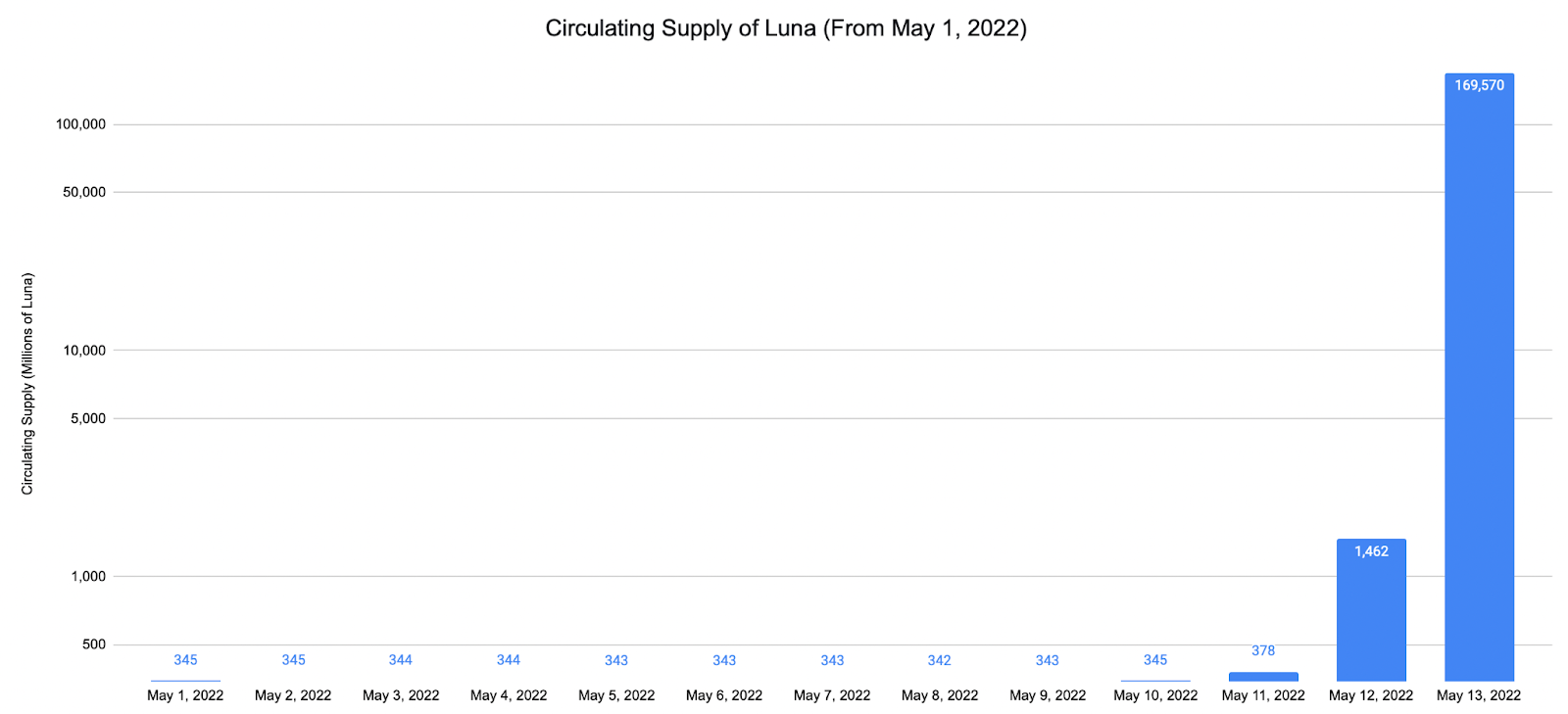

LFG minted an unbelievable amount of LUNA tokens to decrease UST’s circulating supply and push its value back to the $1 peg.

LUNA’s one billion total supply rose to 6 billion on May 10, more than 50 billion on May 11, and over 6 trillion tokens by May 13.

The below chart displays the massive spike in LUNA’s circulating supply which was minted in a matter of three days.

Source: Messari

In the end, none of this LUNA printing could save the value of UST which fell to as low as 10 cents per token on May 13 when the Terra blockchain was finally halted. Hyperinflation collapsed the price of LUNA from $60 to less than one cent within a few days, and exchanges simultaneously stopped both Luna’s and UST’s trading activities.

The aftermath

The collapse of LUNA and UST created insolvencies among major crypto hedge funds and venture capital firms, some of which ended with bankruptcy.

One of the largest crypto hedge funds, Three Arrows Capital (3AC) filed for bankruptcy in June following a British Virgin Islands (BVI) court order that liquidated the fund’s BVI branch assets. The liquidation order came after 3AC defaulted on a $650 million loan from digital asset brokerage Voyager Digital on June 27. The major trigger for this insolvency was 3AC’s $560 million long position in LUNA, which practically went to zero with Terra’s collapse.

Voyager Digital also filed for bankruptcy in the next few weeks.

On May 27, the Terra blockchain was forked by the order of a community vote. The new chain, Terra 2.0 or Terra, replaced the old one (now called Terra Classic) and exists without UST. Many of the apps and protocols that existed on the now-Terra Classic carried over to Terra 2.0.

Despite offering similar utilities for users as Terra Classic did before the collapse, the updated network has so far failed to gain traction. Terra 2.0 captured about $270 million in value as of June 30. This represents a near 82.5% drop since it went live in late May.

Ethereum block space wars

Network miners or validators on a blockchain compete for block space, which is the right to create new blocks. Earning block space requires a certain amount of investment – either in the form of computing power, as with mining, or by having a stake in the network’s native currency, which is required of validators. When a new block is created, miners or validators earn rewards as a return for their investment.

The Ethereum network has been the site of the most fierce block space wars in the cryptocurrency ecosystem. This is a consequence of Ethereum’s scaling issues that have persisted since its launch.

The low throughput of the original Ethereum blockchain (15 transactions per second) causes the network to get congested very easily. The demand by users to be included in the next validation block on a highly congested network typically causes miners to demand astronomical transaction fees, also known as gas.

Layer 2 (L2) protocols were introduced on Ethereum as a scaling solution. L2 protocols act as side roads from the main Ethereum network to execute transaction requests. This in return reduces the load on the mainnet (layer 1, or L1) and makes transactions cheaper and faster.

On an L2 network, transactions are recorded “off-chain” without being acknowledged by the main, L1 network. A user can execute any number of transactions on L2 while paying for a single on-chain transaction (gas) on the mainnet.

Fees on L2 networks are typically very low and the subsequent drops in on-chain transaction loads significantly reduce the gas fees on the main Ethereum blockchain.

The share of Ethereum transactions on the mainnet has been diminishing against transactions on Optimism and Arbitrum, two of the leading Ethereum L2 solutions. Making up less than 4.5% of all Ethereum transactions as of 2021’s end, transactions on Optimism and Arbitrum occupy more than 35% as of Q2 2022.

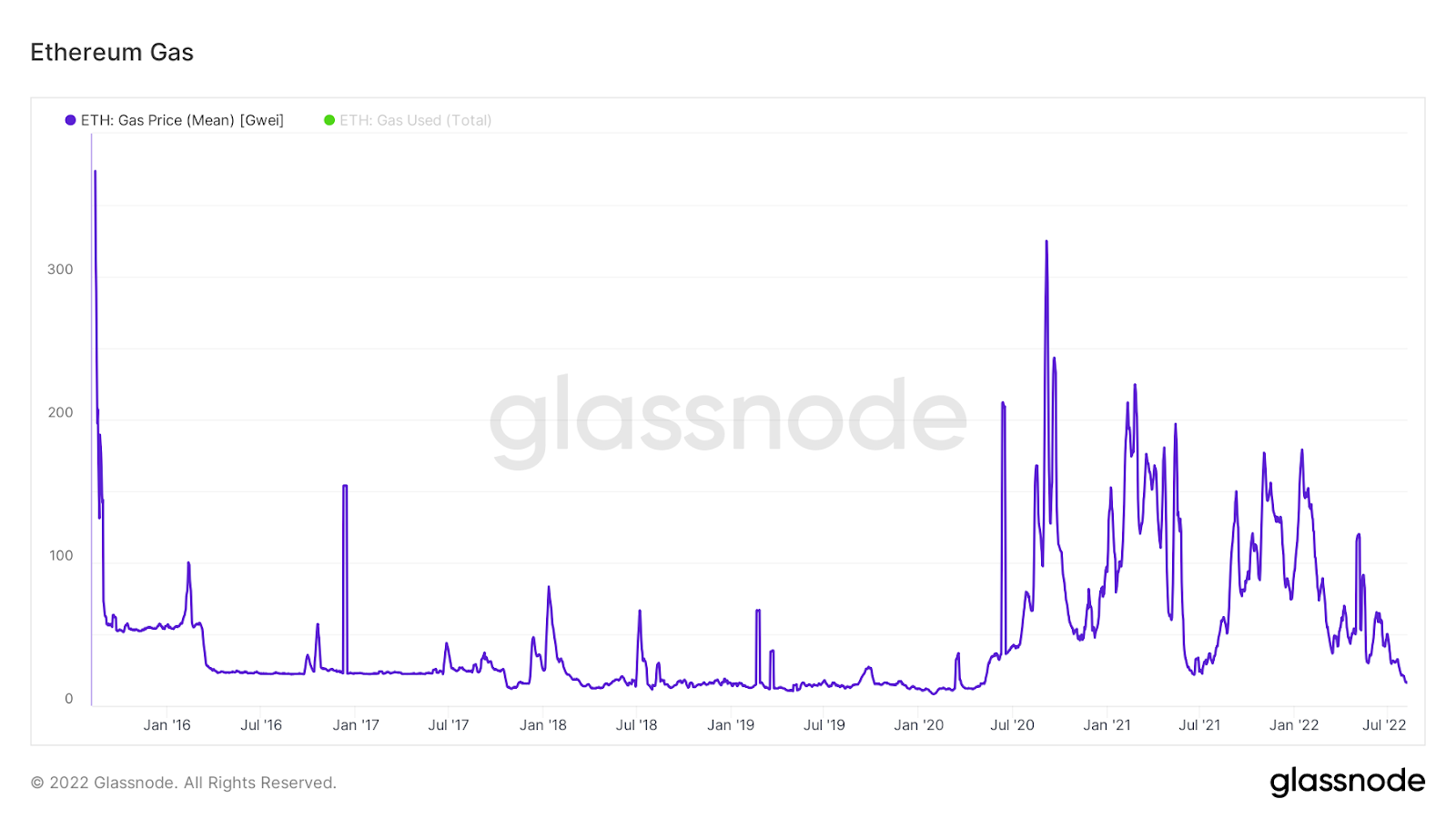

This means 35% of the entire Ethereum block space is consumed by L2 protocols. The decline in mainnet activity significantly dropped the network revenue which resulted in massive Ethereum deleveraging during the first half of 2022. The price of Ethereum dropped from $3,500 in December 2021 to as low as $900 on June 18. During this period, the average gas fee on the mainnet dropped from over $200 in 2021 to $30 on June 19.

Ethereum gas price chart. Source: Glassnode

Decoupling of stETH from ETH

stETH, Ethereum’s liquid-staking token that acts as a proxy to ETH, lost its peg against ETH on May 9, amidst Terra’s collapse. stETH’S main liquidity pool on the Curve platform lost more than half of its TVL in only three days (from $4 billion on May 9 to $1.9 billion on May 12). As a consequence, the value of stETH cratered to 0.88 per ETH coin on May 13.

Liquid-staking provides liquidity for staked assets by creating proxies of those assets. Where staked tokens are typically rendered illiquid since they are locked on the blockchain of their native cryptocurrency network, these proxies give users full mobility while continuing to earn rewards. This in return encourages growth on the network where locking assets once limited their utility.

Liquid-staking tokens like stETH typically hold similar utility to the underlying staked asset (ETH) and can be deployed concurrently in order to bring liquidity to the ecosystem.

Normally, liquid staking tokens can be swapped with the base staked asset which immediately releases the lock on the staked token. However, on the Ethereum network, the ETH locked in staking contracts is inaccessible until an unknown date after the “Merge.”

Considering that, most people use stETH tokens only for leveraging their ETH staking rewards by swapping the two tokens back and forth. Overleveraging for maximum rewards eventually created an imbalance in the stETH/ETH liquidity pools, where there was not enough ETH to withdraw during turbulent times like the panic selling event in May 2022.

For example, Celsius, once a major player in the crypto lending market, used to receive ETH deposits from its customers and liquid-stake them through Lido, the original issuer of stETH. Back in May, the company had over 400,000 stETH.

However, there were only 148,378 ETH in the stETH/ETH Curve pool to exchange for 400,000 stETH tokens. As a result, Celsius was unable to dispose of the total stETH they own for ETH even after draining the pool’s entire liquidity. This triggered a bank run for Celsius and panic selling for stETH. Eventually, the stETH/ETH peg broke and the parity traded at 0.88 on May 13.

The result was a huge liquidation event for stETH collaterals on DEXs and lending platforms. As stETH tokens have generally been used for leveraging, their depeg from ETH can be considered another major catalyst in the DeFi market’s massive deleveraging in 2022.

More storms ahead?

The second quarter of 2022 was characterized by adverse events that vanished the bulk of the DeFi market’s progress since 2020. Taken together, these three events help explain DeFi’s slump over the last quarter.

Will the market see more de-pegs, block space wars, bankruptcies, and forced liquidations this quarter?

While black swan events have been commonplace in the crypto world since day one, the ecosystem continues to bounce back, and often reaches new horizons. People who believed in the long-term value and use cases of crypto products have generally been the ones that achieved the maximum returns in the cryptocurrency economy.

Although such events could repeat, the massive deleveraging that took place in the DeFi space – from $180 billion to $52 billion – could allow breathing room this quarter to pump some liquidity and leverage back into the system.

Keep your eyes out for further updates and analysis from CEX.IO as the crypto ecosystem continues to evolve. To always stay informed, follow us on social media, or sign up for our mailing list to never miss a beat.

Disclaimer: Information provided by CEX.IO is not intended to be, nor should it be construed as financial, tax or legal advice. The risk of loss in trading or holding digital assets can be substantial. You should carefully consider whether interacting with, holding, or trading digital assets is suitable for you in light of the risk involved and your financial condition. You should take into consideration your level of experience and seek independent advice if necessary regarding your specific circumstances. CEX.IO is not engaged in the offer, sale, or trading of securities. Please refer to the Terms of Use for more details.