- Both crypto fundraising and M&A reached an all-time high in 2025 in terms of volume.

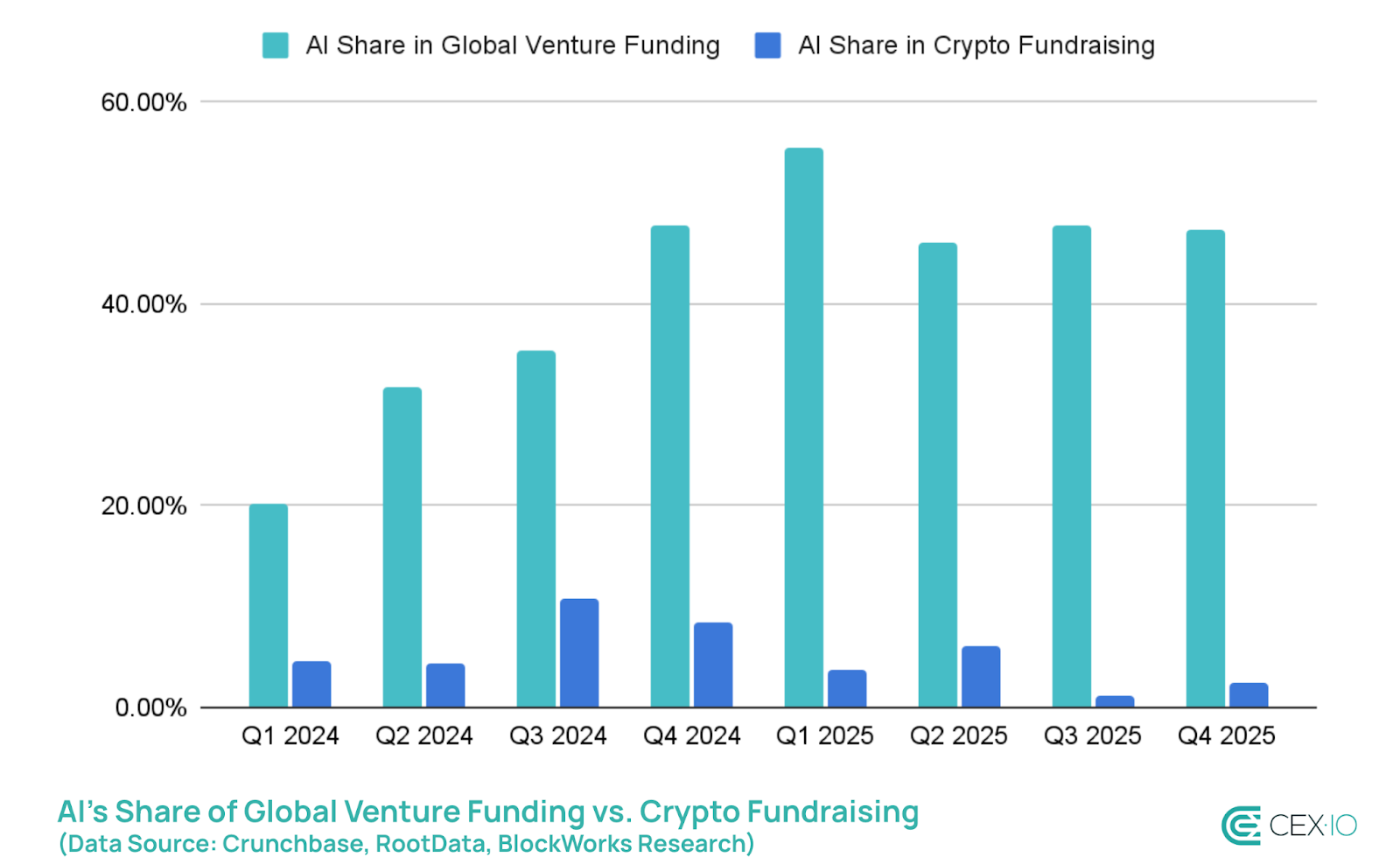

- While other industries double down on AI, its share within crypto fundraising dropped nearly 3 times in 2025.

- 2025’s largest deals were primarily M&As, IPOs, and strategic investments from traditional financial institutions.

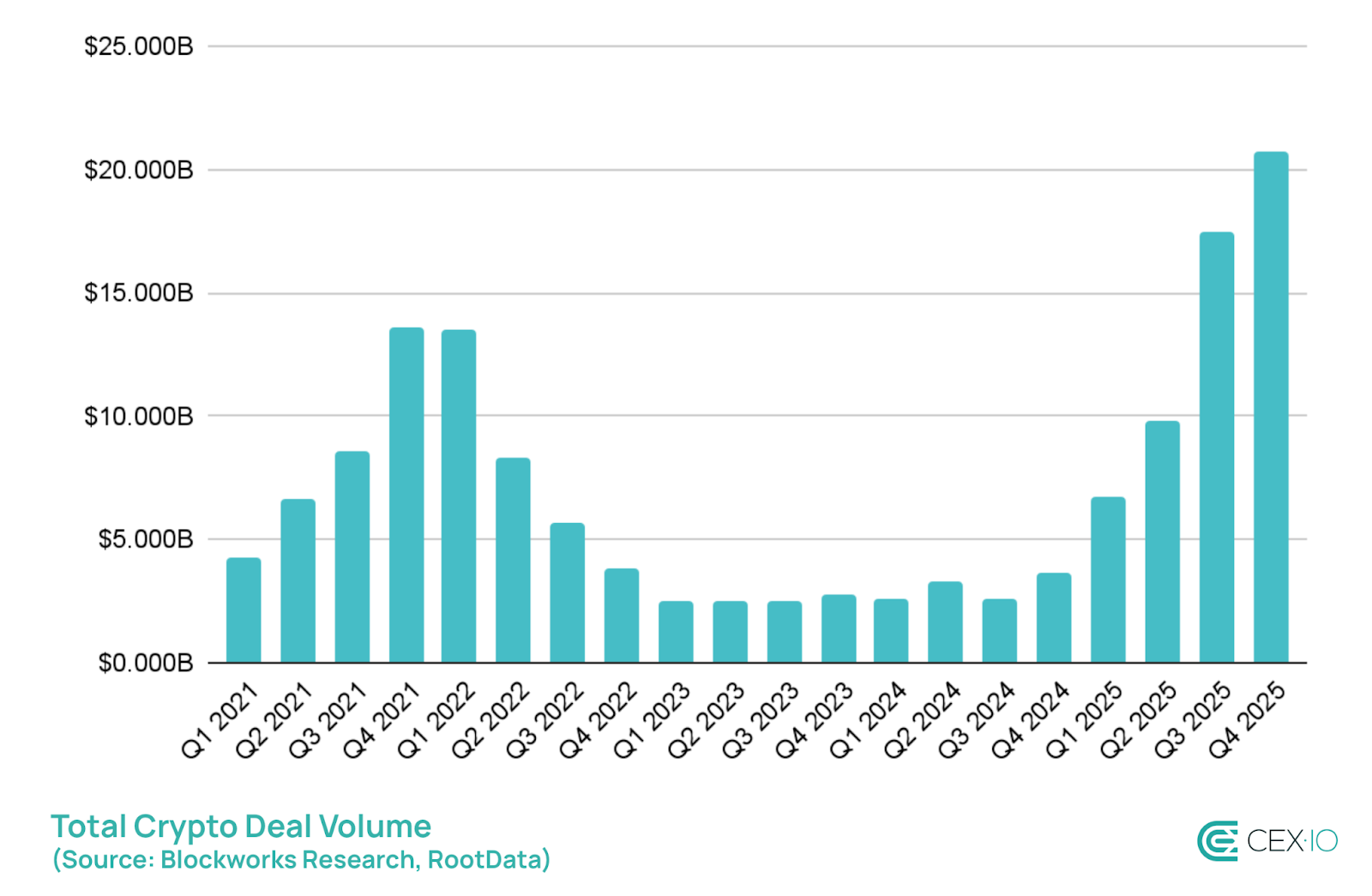

2025 marked a historic year for crypto dealmaking, with combined fundraising and M&A activity reaching nearly $55 billion. The momentum peaked in Q4 2025, which emerged as the busiest quarter the industry has ever recorded. Landmark events included Naver’s $10 billion merger with Dunamu, Polymarket’s $2 billion raise led by Intercontinental Exchange, and Kalshi’s $1 billion fundraising round, which collectively drove this record-breaking quarter.

Compared to 2024, the scale of crypto deals jumped by 350% in 2025. This surge in activity was so unprecedented, nine of the ten largest crypto deals in history took place last year. The only exception within the top ten remains EOS’s $4 billion ICO in 2018, which still stands as the largest ICO ever.

2025’s largest deals were primarily M&As, IPOs, and strategic investments from traditional financial institutions, highlighting the industry’s maturation and its deepening integration with the broader financial system.

Crypto Fundraising Is Among Leading Sectors in Global Funding

Crypto fundraising reached $35.6 billion in 2025, surpassing the previous peak in 2021 and setting a new all-time high. Considering Crunchbase estimates of global venture funding last year, this would position crypto among the leading funded sectors, behind AI and healthcare/biotech.

One of the most notable divergences between crypto and broader venture markets is its declining exposure to AI. While AI accounts for roughly half of all global venture funding, its share within crypto has continued to shrink, falling from 7% of total crypto fundraising in 2024 to just 2.6% in 2025.

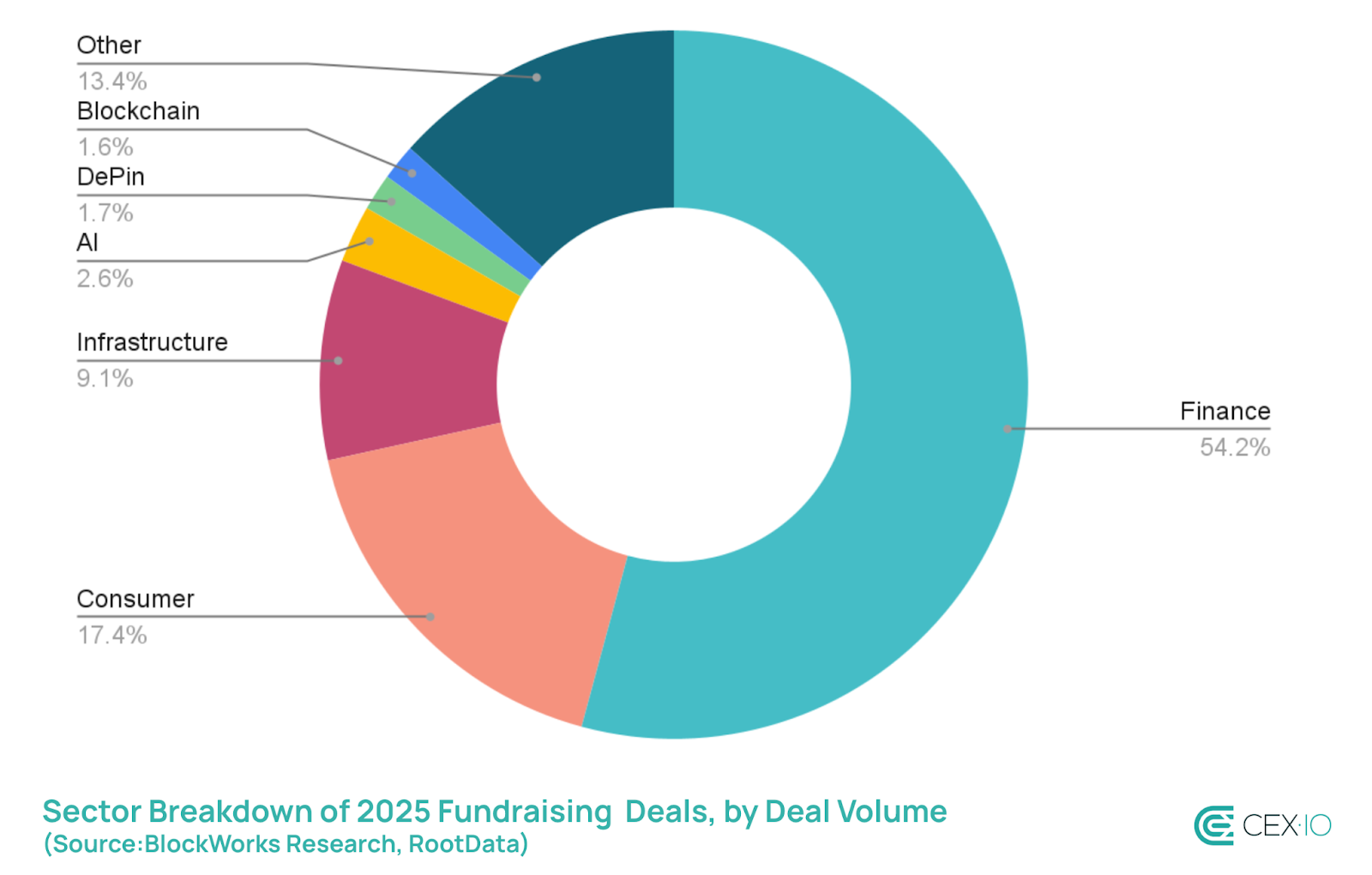

Instead of AI, the majority of funds in 2025 was allocated to finance-related projects (exchanges, stablecoins, tokenization, etc.), totaling more than $19 billion. Consumer apps (prediction markets, gaming, wallets, etc.) came second with over $6 billion, while infrastructure (hardware, security tools, bridges, etc.) rounded out the top three with over $3 billion.

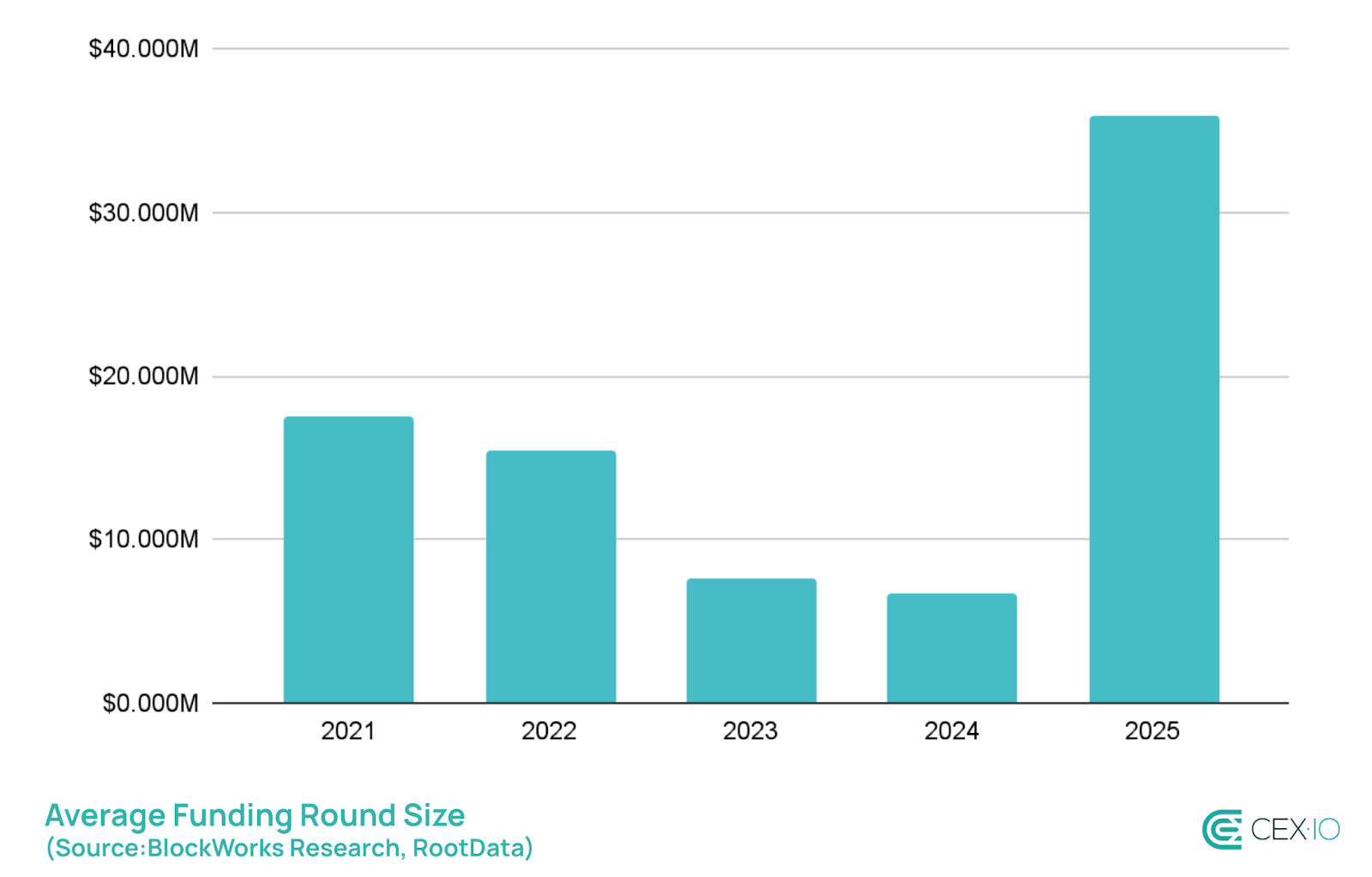

Another distinctive aspect of 2025 was fundraising distribution. Rather than scattering investments across numerous small projects, VCs are now writing bigger checks to fewer companies. The deal count fell by 36% year-over-year, while the average round size climbed to nearly $36 million, signaling a clear preference for quality over quantity.

This dynamic mirrors a broader trend across the fintech sector last year, where deal count declined by 23%, even as total deal volume increased by 27%. However, the average fintech round size stood at roughly $15 million in 2025, or about 2.4x smaller than in crypto, highlighting crypto industry’s continued appeal.

Crypto M&As Became More Common and Pronounced

In 2025, the crypto industry experienced an unprecedented and rapid rise in M&A volume and count. First of all, it’s important to point out that M&A data is less transparent than fundraising. While 140 crypto M&As were recorded in 2025, about 86% of them did not disclose the transaction amount, making it difficult to estimate the true value of the sector’s activity.

Still, deals with publicly disclosed values have exceeded $18 billion, representing more than a 10x increase from 2024. For comparison, global M&A value reportedly rose by 40% in 2025.

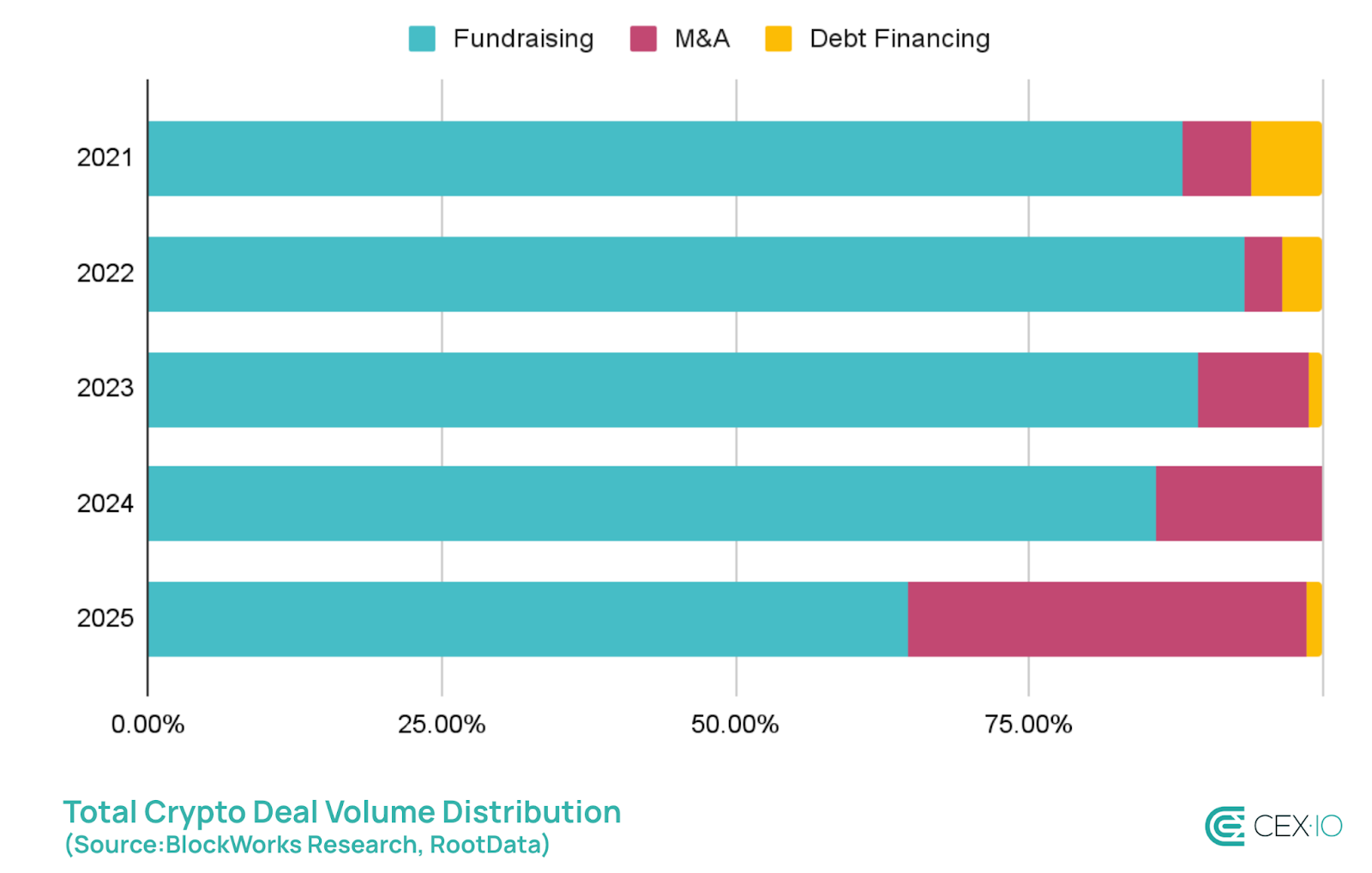

As a result, M&A now makes up 34% of total crypto deal volume, the largest proportion ever recorded.

This surge in acquisitions signals market maturation. Companies are increasingly buying rather than building, acquiring existing technology, talent, and user bases to accelerate growth. The move from pure innovation to strategic consolidation suggests the industry is entering a new phase of development.

Similarly to fundraising, most of the known deals are in the Finance sector, accounting for 96% of volume and 46% deal count. Notable examples include Coinbase purchasing Deribit, Kraken acquiring NinjaTrader, and Ripple buying Hidden Road.

2026 Outlook

The trends established in 2025 are likely to persist throughout 2026, but the scale of crypto deals may go down similarly to 2022 if broader market conditions deteriorate.

M&A activity will likely accelerate as the industry continues maturing. Larger players with strong balance sheets will use market downturns as opportunities to consolidate smaller competitors or acquire strategic technologies at more favorable valuations. At the same time, fundraising patterns will probably mirror 2025’s evolution toward fewer but larger rounds in general.

Most likely, Finance will remain the dominant category for crypto deals in 2026, with stablecoins, tokenization, and new CeFi/DeFi projects among the most promising subcategories. Stablecoin volume and supply have been actively increasing throughout 2025, and newly established regulatory frameworks like the Genius Act could encourage TradFi to explore stablecoin infrastructure more actively.

Tokenization and RWAs have been one of the fastest growing sectors in DeFi this year, primarily due to increased adoption of tokenized treasuries/gold/stocks, as well as private credit. This category is particularly attractive to investors because it serves as a practical bridge between TradFi and crypto. On one side, it introduces crypto users to conventional asset classes. On the other, it offers traditional investors an opportunity to benefit from 24/7 trading, fractional ownership, and faster settlement times.

Overall, 2026 will likely see an even more selective, strategically-focused crypto investment landscape than in 2025.

Sources

The data used for this research consists of publicly available information from RootData, Blockworks Research, Crunchbase, Lazard, and Coingecko. The observation period for this study was focused on 2021-2025 for general overview, and 2025 for sector overview, with data points ending January 1, 2026.

The web content provided by CEX.IO is for educational purposes only. The information and tools provided neither are, nor should be construed as, an offer, or a solicitation of an offer, or a recommendation, to buy, sell or hold any digital asset or to open a particular account or engage in any specific investment strategy. Digital asset markets are highly volatile and can lead to loss of funds.

The availability of the products, features, and services on the CEX.IO platform is subject to jurisdictional limitations. To understand what products and services are available in your region, please see our list of supported countries and territories. This page includes additional links to information about individual products, and their accessibility.